April and National Financial Literacy Month are in the rearview mirror. But that doesn’t we should take our feet off the gas pedal when it comes to addressing the nation’s financial literacy epidemic. According to our annual CPA/Wealth Advisor Confidence Survey, just one-third of financial advisors (38%) believe America’s financial awareness has improved in the two years since COVID surfaced – and they’re particularly worried about the lack of money skills among Millennials and Gen Z.

“One positive that came out of the pandemic is the spotlight on personal finance as an important lifelong skill for everyone,” said respondent Marie Burns a financial advocate. “Now more states than ever are proposing legislation to teach financial literacy in schools.” Once again, our survey respondents felt K-12 schools could make a bigger impact on America’s financial literacy than any other institution in our society.

But who knows how to teach financial literacy?

As a result of the school system’s lack of modernization, survey co-author Valentino Sabuco, Executive Director of The Financial Awareness Foundation, said experts who teach financial literacy are few and far between. “Many teachers unfortunately lack the knowledge themselves on financial literacy,” said Sabuco. “They are ill prepared to teach it to the next generation of students. For those that say they are teaching personal finance, we ask them: ‘Are your materials up to date? Are you touching all the bases?” More often than not, the answer is NO, lamented Sabuco.

Jim Stovall, motivational speaker and author of Millionaire Map told us that there is more information than ever about financial awareness, but we are bombarded with confusing, mixed messages as not all information is accurate and valid. “It’s not a matter of getting information, it’s a matter of getting the right information,” said Stovall.

According to Sabuco, many educators believe financial literacy only deals with savings, budgeting and debt management. They don’t address ways to help students get and stay organized, establish personal and financial goals, save for college or plan for other major expenditures such as cars and house down-payments. “So how do financially illiterate teachers successfully teach personal finance to students?” asked Sabuco.

Dr. Guy Baker, CFP, Ph. D, founder of Wealth Teams Alliance in Irvine, California told me quite simply that most Americans are financially illiterate. “A home economics course should be a core class for high schoolers,” said Baker. “It needs to teach students how to bank, how to save, how to invest and how to use a credit card.” Baker said it should teach them about buying a home vs. renting, buying a car. In other words, “All of the essentials responsibilities that are required to live a productive life.”

Dr. Christopher Sparks, Ph. D, of Academic Investment Management thinks there may be too many constraints on public schools to teach financial literacy effectively and that colleges and universities, may be better equipped. He’d also like to see financial advisors more involved with teaching financial literacy to the masses, but they tend to target those with significant investable assets. “Those who don’t have much to invest are largely ignored,” Sparks observed.

The simple answer to this complex question, said Sabuco, is to provide our youth with the “necessary life skills and problem-solving skills to have the best chance of living a successful life, without outliving their wealth.”

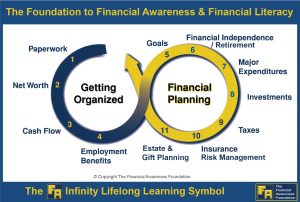

Many of these topics, said Sabuco, are built around the financial elements identified on The FA Infinity Lifelong Learning Symbol shown below

“If all the allied professions (attorneys, CPAs, financial planners, insurance consultants, etc.) took a collaborative and holistic approach, consumers would hear a similar message from several different perspectives and would be more likely to hear the message and act on it,” said attorney Martin M. Shenkman.

Lionel Shipman, a financial and life empowerment professional, told us that financial literacy education should start as early as elementary school. “As children continue their education through middle and high school, their knowledge and experience of financial literacy skills can be broadened and strengthen, preparing them to succeed financially in adulthood,” added Shipman. Ryan Vogel, CFP, Partner, Chief Planning Officer, Novi Wealth in Princeton, New Jersey, agreed. Even among schools that do have financial literacy requirements, Vogel said teaching good lifelong money habits should be part of ongoing curriculum, not a one-off required course like health or driver’s ed.

“In addition to teaching it in high school, there should be a more basic version taught in middle school and some type of financial literacy curriculum in 4th or 5th grade to get them started on the right path,” suggested Vogel.

Conclusion

Bottom line: Everyone from early childhood educators to high schools and university instructors, financial advisors, spiritual advisors and most importantly, parents setting a good example for their children, need to do their part. “We must change the system to help all children from a very young age to develop the financial literacy skill so that it will be part of their lifelong DNA,” said survey respondent Elena Zee, President & CEO Arizona Council of Economic Education (ACEE). Curing the financial illiteracy epidemic in this country takes a village. Are you willing to step up?

Don’t agree? Tell me why.

Here’s how you can support the people of Ukraine

TAGS: #financialliteracy, #financialawareness, #financialeducation, #smartmoney